Flying in turbulent times – the voluntary administration of Virgin Australia

By Mark Petrucco, Katherine Payne, Megan Scott and Camille Gray

In what has been Australia’s largest corporate scalp in the wake of the COVID-19 pandemic, Virgin Australia has appointed partners from Deloitte as voluntary administrators. The decision to appoint administrators reportedly arose from the Federal government’s refusal to inject $1.4b as part of a recapitalisation proposal.

For many, including creditors, customers and businesses who had dealings with Virgin Australia, the appointment will bring an air of uncertainty and turbulence to the future of Australia’s second largest airline. It may be a sense of déjà vu for some, almost two decades after the then second largest airline, Ansett Australia, collapsed and was subsequently liquidated.

So what happens during the voluntary administration process? In this article, we provide a brief overview of the process, and share our comments on the possible outcome of the administration process.

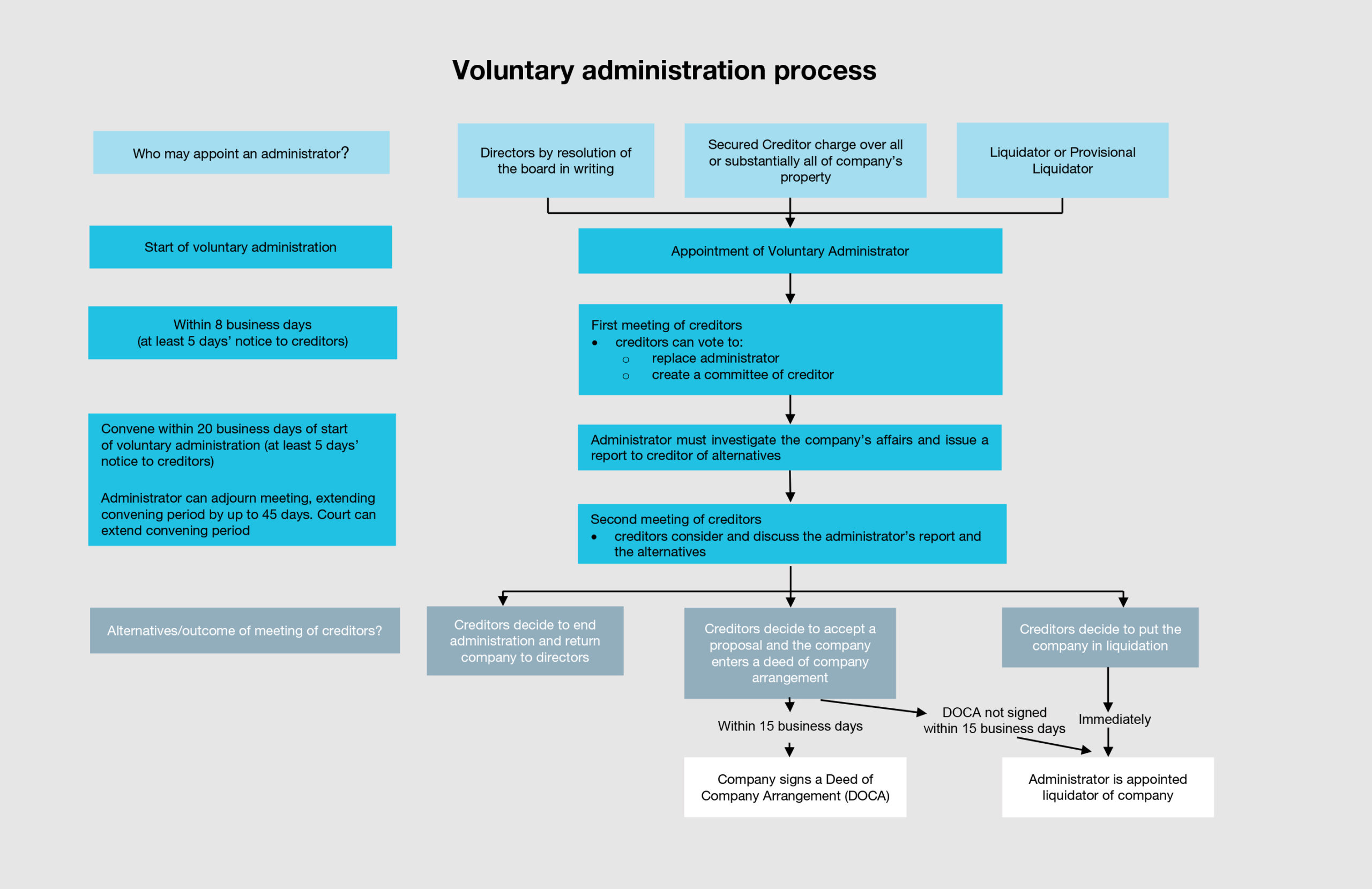

Appointment of Administrators

The appointment of a voluntary administrator is generally made under section 436A of the Corporations Act 2001 (Cth). That provision provides that a company may appoint an administrator if the board of directors has resolved that in their opinion the company is insolvent or is likely to become insolvent at some future time, and that an administrator should be appointed to the company.

Purpose

The purpose of the voluntary administration process is to assess whether a financially distressed business can be rescued or restructured, and if not, it is designed to maximise the return to creditors compared to an immediate liquidation.

Who controls the company in voluntary administration?

Once an administrator is appointed, the powers of directors are suspended unless the administrator gives them specific approval. The administrator takes control of the company’s property and business, and will decide whether to continue to trade the business.

The directors are required to assist the administrator, in particular with regard to the administrator’s investigations and preparation of a report as to the company’s affairs, and by delivering the company’s books and records to the administrator. In large administrations such as Virgin Australia, it is typical that senior management will work closely with the administrators during the administration period.

Claims against the company in voluntary administration

During the administration, creditors cannot start or continue legal action against the company or its property without the administrator’s consent or leave of the Court.

Generally, secured creditors are restricted from enforcing their security interest during the administration period, unless they have security over the whole, or substantially the whole of the property of a company. In that case, secured creditors are given 13 business days from the commencement of the administration to decide whether to enforce their security. Typically, this would involve appointing a receiver (another specialist insolvency accountant) to manage the property or business subject to the creditor’s security interest. Creditors who hold personal guarantee(s) from or on behalf of the directors cannot enforce those guarantees during the administration process.

Under recent ‘ipso facto’ law reform, a party to a contract with a company in administration entered into after 1 July 2018 cannot exercise termination, enforcement or other contractual rights for the sole reason that it has had an administrator appointed. However, that party does not have to continue to provide credit to the company in administration, and for example, can insist on ‘cash on delivery’ under a supply contract. These laws are designed to preserve the corporate value by retaining contracts that are in place and consequently improve the administrators’ prospects of achieving a viable restructure of the company and return to creditors.

Timing of the voluntary administration process

A flow chart outlining the voluntary administration process is at the end of this article.

First meeting

A meeting of creditors must be held within 8 business days after the administration begins. The administrator must prepare an initial report to creditors ahead of the meeting. At this first meeting, the creditors decide whether a committee of inspection should be appointed (which is typical for large corporations such as Virgin Australia) and whether the current administrator should be replaced with another.

Role of the committee of inspection

The committee of inspection is generally formed of the company’s creditors, and will commonly include a representative for employees and the major creditors. Members appointed to the committee represent the interests of all creditors. The committee plays a consultative role for the administration process and can give limited directions to the administrator on behalf of the creditors. Often the administrator will consult with the committee regarding major decisions in the administration, but the administrator remains independent and is not obliged to follow any directions from the committee.

After first meeting and before second meeting

In large administrations, the administrators and their staff undertake multiple streams of work, which for Virgin Australia may include:

- continuing to trade the business at a reduced operational capacity, reflecting the restrictions arising from the COVID-19 pandemic. This would be done with the assistance from existing Virgin staff who have the operational experience;

- assessing the ongoing viability of the business to see whether it can be rescued or restructured. Often this requires working closely with corporate advisors, existing financiers and major shareholders. Media reports suggest the administrators have commenced an expression of interest campaign aimed at finding a buyer for the business. Buyers may include existing financiers and shareholders, other airlines, and investment funds;

- investigating the company’s business, property, affairs and financial circumstances. This will include investigating whether there are any uncommercial transactions or conduct of the directors which may form the basis of a recovery action if the company goes into liquidation; and

- setting out the terms of any proposal that the company enter a deed of company arrangement, which would compromise unsecured creditor claims.

The administrators must then form an opinion about each of the following matters:

- Whether it would be in the creditors’ interests for the company to execute a deed of company arrangement (DOCA) (discussed further below);

- Whether it would be in the creditors’ interests for the administration to end; and

- Whether it would be in the creditors’ interests for the company to be wound up (ie placed into liquidation).

Second meeting of creditors

The administrator is required to convene a second meeting of creditors within 20 business days of the start of the administration (the convening period), and must hold the meeting within 5 business days before or after the end of convening period. If further investigations or negotiations are required, the administrator can either (i) apply to the court for an extension of the convening period; or (ii) if only a short extension is required, the administrator (or by resolution of creditors) can adjourn the second meeting, effectively extending the convening period to 45 days. Given the size and likely complexity of Virgin Australia’s administration and the ongoing restrictions due to the pandemic, the administrators have indicated that they expect the administration process to take two to three months. We anticipate the administrators will apply to the Court for an extension of the convening period and the holding of the second meeting of creditors.

Accompanying the notice of the meeting sent to creditors is the administrator’s report discussing the company’s business, property, affairs, reasons for its failure and financial circumstances. The notice also includes a statement setting out the administrator’s opinions on the above three matters (ie. whether it would be in the creditor’s best interests to vote for a proposed DOCA, end the administration, or appoint a liquidator) and their reasons for those opinions. If a deed of company arrangement is proposed, the administrator must set out the details of the proposed deed.

The second meeting of the company’s creditors is important as it decides the fate of the company. At this meeting the creditors may decide either:

- that the company execute a DOCA specified in the resolution;

- that the administration should end and that the company be returned to the directors; or

- that the company be placed in liquidation.

A resolution of creditors will carry if a majority in number of creditors vote in favour of the resolution and the value of the debts of those voting in favour of the resolution is more than half the total debts of the company.

Employee entitlements and meeting

Outstanding employee entitlements receive a priority treatment in the ranking of payments in a liquidation scenario. If a proposed DOCA concerns the distribution of outstanding employee entitlements, those employee entitlements must rank at least equal to the priority they would receive in a liquidation scenario.

If the proposed DOCA does not contain an equal priority for these entitlements, the administrator must convene a separate meeting of employees to seek their approval. Notice of the meeting must be accompanied by a statement setting out the administrator’s opinion as to why the proposed DOCA will result in a better outcome for employees than they would otherwise receive in an immediate winding up of the company. The Court also has the power to approve a DOCA where employee entitlements do not receive an equal priority treatment.

Secured creditor rights

During the administration process, while secured creditors cannot enforce their security interest (subject to the exception discussed above), the administrator generally cannot dispose of the secured property without the consent of that secured party or court approval (unless that disposal is in the ordinary course of business). Any net proceeds of the sale of the secured property must be applied towards payment of the debt secured by the security interest.

Deed of Company Arrangement

A DOCA is a deed entered into by the company and the administrator (who generally becomes the ‘deed administrator’), which binds all unsecured creditors as at the date of the appointment of the administrator. In the case of Virgin Australia, that date is 21 April 2020. Secured creditors are not bound by the deed unless they voted in favour of it at the second meeting, or the court orders them to be bound. The deed must be signed within 15 days of the creditor’s resolution made at the second meeting, otherwise the voluntary administration will end, and the company will be deemed to be wound up voluntarily (ie. put into liquidation).

Once executed, the company and the deed administrator must perform the terms of the deed. It is at this point that control of the company usually returns to the directors, although this is subject to the terms of the deed. What is required under the deed will depend on its terms, but often they are used to create pools of funds such as contributions made by stakeholders or the proceeds of sale of the company’s assets. The funds are then distributed to unsecured creditors over a period of time and in such proportion in accordance with the deed. One major benefit of using a DOCA is that, in the right circumstances, it can allow the company and the deed administrators to achieve a more orderly and better sale outcome for the company’s business and assets, and therefore higher returns to creditors rather than if there was an immediate liquidation.

Possible outcome?

It is too early to speculate on the likely outcome of the Virgin Australia administration. Early media reports suggest that up to 10 interested buyers have already expressed interest in the Virgin Australia business, which is a positive early sign for the future of the airline. How this will affect creditors (including customers with booked flights, or who hold credits from cancelled flights) is unknown at this point.

If no suitable buyer or equity capital is found, Virgin Australia will likely be forced into liquidation.

The Federal Government has so far declined to provide financial assistance to Virgin Australia. Treasurer Josh Frydenberg has specifically cited the fact that the airline is 90% owned by 5 large foreign shareholders ‘with deep pockets’. It is unclear whether this position will be maintained during the course of the administration as the search for the recapitalisation of the group continues. The Australian market needs and can support a two airline market, and the Federal Opposition is calling for the Government to take an equity stake in the airline in order to support this. The very real prospect of having only one major airline operate in Australia, with no competition, is a position that the Federal government does not want to see.