Marshalling: how it can help a second mortgagee

What is it?

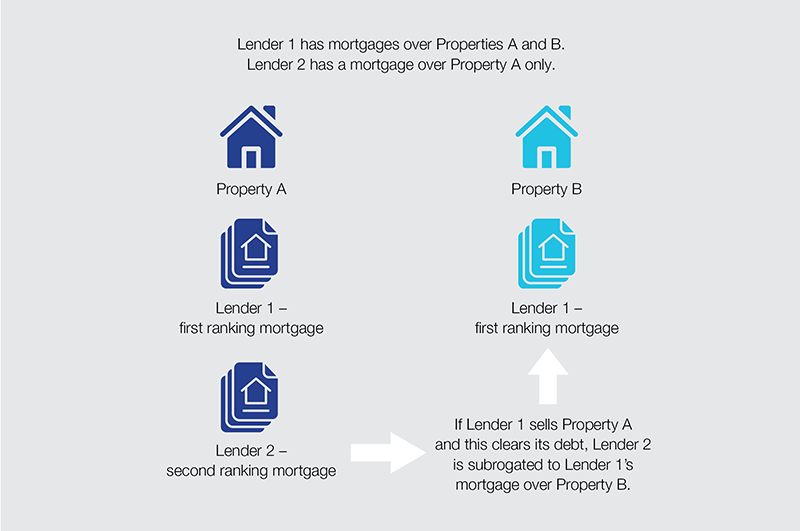

The equitable doctrine of marshalling of mortgages allows a second mortgagee whose debt has not been paid from the sale of mortgaged property to access the proceeds of sale of another property mortgaged by the same debtor to the same first mortgagee, even though the second mortgagee has no security over that property.[1]

Practically, the doctrine protects the second mortgagee from the first mortgagee’s decision to sell the commonly mortgaged property rather than a property only mortgaged to the first mortgagee.

The diagram below illustrates how the doctrine operates.

When is it available?

The Supreme Court of the United Kingdom recently summarised the marshalling doctrine in the case National Crime Agency v Szepietowksi.[1] Lord Neuberger determined that marshalling may be available to a creditor in circumstances where the:

- creditor’s debt is secured by a second mortgage over property (Common Property);

- first mortgagee of the Common Property is also a creditor of the debtor;

- first mortgagee also has security for his debt in the form of another property (Other Property);

- first mortgagee has been repaid from the proceeds of sale of the Common Property;

- second mortgagee’s debt remains unpaid; and

- proceeds of sale of the other property are not needed to repay the first mortgagee’s debt.

If these criteria are satisfied the second mortgagee can look to the other property to satisfy the debt owed to it.

Why is it useful?

Marshalling rights are primarily relevant in circumstances where the debtor is insolvent. This is because marshalling improves the position of the second mortgagee against the unsecured creditors of the debtor, however, it does not improve the second mortgagee’s position against the debtor themselves or the first mortgagee.[2]

The doctrine has no effect on the first mortgagee’s rights.

Practical example

Here is an example of circumstances where marshalling significantly improves the return to the second mortgagee:

- A mortgagor owes $2 million to the first mortgagee and $2 million to the second mortgagee.

- The Common Property (mortgaged to the first and second mortgagees) and the Other Property (mortgaged only to the first mortgagee) are worth $3 million each.

- The Common Property is sold for $3 million resulting in repayment in full of the debt owed to the first mortgagee and a reduction of $1 million in the debt owed to the second mortgagee.

- The mortgagor still owes $1 million to the second mortgagee, whether or not the second mortgagee can marshal.

- The effect of the second mortgagee being able to marshal is that it can directly enforce its outstanding $1 million debt against the Other Property rather than being a mere unsecured creditor. The second mortgagee can step into the first mortgagee’s shoes and exercise its mortgage over the Other Property.

Court of Appeal decision – Burness v Hill [2019] VSCA 94

This case considered the equitable doctrine of marshalling of mortgages and whether a second mortgagee lost any marshalling rights by various defences raised on behalf of the unsecured creditors by the trustees of the bankrupt estate of the debtor.[3]

Grounds of appeal

Mr Love was the registered proprietor of three properties in Epping and executed mortgages over each piece of land in favour of the Commonwealth Bank of Australia (CBA). Mr Love owed fees to his solicitor Mr Hill and created a second mortgage to Mr Hill over the first property as security for Mr Hill’s outstanding fees.

Mr Love defaulted under the mortgage to the CBA who sold the first property. After the sale of the first property, Mr Hill brought a proceeding in the County Court of Victoria against Mr Love for payment of outstanding fees (County Court Proceeding). The County Court Proceeding was settled at mediation and resulted in a judgment for Mr Hill against Mr Love for $2.2 million. [4] The second and third properties were sold after the judgment was obtained.

The proceeds of the first and second properties were insufficient to discharge the indebtedness to the CBA. However, the sale of the third property resulted in a full payout to the CBA.

Mr Hill subsequently commenced proceedings in the Supreme Court and relied on the doctrine of marshalling to obtain the surplus proceeds of sale of the third property (i.e. after provision had been made to the CBA). Mr Love was made bankrupt by a sequestration order during the proceeding and he later passed away on 1 April 2016.[5]

Decision at first instance

The Proceeding was tried in the Commercial Court by Sifris J for a period of five days in September 2017. Sifris J delivered a judgment in favour of Mr Hill and made declarations and orders upholding his right to marshal to the surplus proceeds of sale of the third property (to the extent of the value of the first property).[6]

In forming his judgment Sifris J dismissed several arguments raised by Mr Love’s trustees in bankruptcy (Trustees). These arguments (which are detailed below) formed the basis of the appeal by the Trustees.

Grounds of appeal

The Trustee’s application for leave to appeal relied on the following grounds:[7]

- There was no secured debt due by Mr Love to Mr Hill at the time the first mortgagee chose to sell the commonly mortgaged property so the doctrine of marshalling could not operate.

- The fact that there was a non-binding agreement between the CBA and Mr Love to sell the first property first destroyed the application of the marshalling doctrine.

- The terms of the settlement of the County Court Proceeding released Mr Hill’s right to marshal.

- Mr Hill acted unreasonably in not raising the marshalling doctrine in the County Court Proceeding.

Decision on appeal

Kaye, McLeish and Hargrave JJ ruled in favour of Mr Hill and held that none of the proposed grounds of appeal were made out. In doing so the Court of Appeal dismissed each of the grounds of appeal on the following basis:

- There was always an amount owing to Mr Hill (being unpaid legal fees and disbursements). Further, the extent of the mortgagee’s marshalling right was not limited to the exact amount and legal character of the secured debt at the time the first mortgagee chose to sell the commonly mortgaged property.[8]

- There has to be a contractually enforceable obligation as to the order of the sale of various properties between the mortgagor and the first mortgagee for the right to marshal to be lost.[9]

- The release in the County Court Proceeding was very general in terms and did ‘not go so far as to release any claim or right to marshal’.[10]

- The marshalling claim was irrelevant to the debt claim for payment of outstanding fees and accordingly, it was not unreasonable for Mr Hill not to have made the marshalling claim in the County Court Proceeding.[11]

Contact