Upcoming AML/CTF compliance for the accounting profession

The accounting profession is on the cusp of significant transformation, with less than 12 months until Tranche 2 entities become regulated under the Anti-Money Laundering and Counter-Terrorism Act 2006 (Cth) (AML/CTF Act). This article explores the new AML/CTF regulatory expectations for the accounting profession and outlines key concerns raised by professional industry bodies.

Strengthened AML/CTF regulations

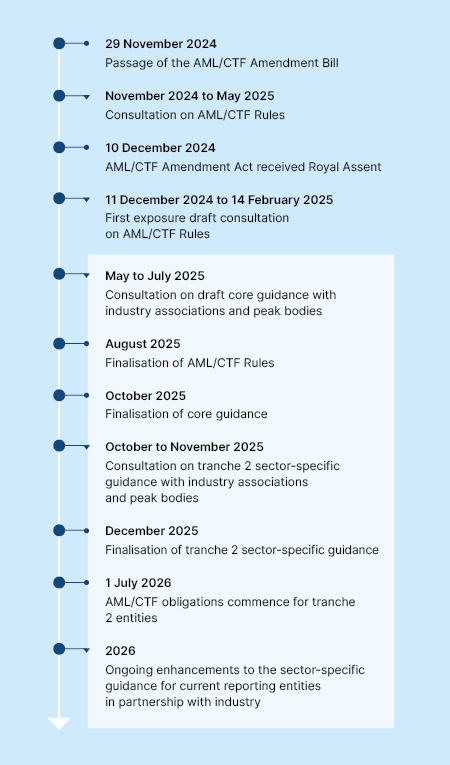

In case you missed it, the AML/CTF Act was passed late in 2024, marking a pivotal shift in Australia’s AML/CTF regime. AUSTRAC is currently consulting with industry associations and peak bodies as part of finalising its re-write of the Anti-Money Laundering and Counter-Terrorism Financing Rules Instrument 2007 (No. 1) (Cth) (Rules). The final draft is expected to be published in late August 2025.

The timeline below provides a snapshot of the key milestones in the reform process.

Which accounting services will be regulated?

It is estimated that the majority of accounting professionals currently, or will, provide the kind of services regulated by the Australian Transaction Reports and Analysis Centre (AUSTRAC) under the new AML/CTF legislative framework, such that they are, or will, be considered Tranche 2 entities.

Those services include:

- assisting with a sale or purchase of an entity

- dealing with money or other property as part of assisting with a transaction

- assisting with an equity or debt financing transaction

- selling a shelf company

- assisting with the creation or restructuring of an entity

- acting as a director, attorney, trustee or similar

- acting as a nominee shareholder

- providing an office address.

AUSTRAC guidance

To provide clarity to accountants and other Tranche 2 entities, AUSTRAC has published guidance on what is expected of regulated entities as the reforms approach, and what regulated entities can expect from AUSTRAC in return. Our recent article, Countdown to AML/CTF reforms: AUSTRAC outlines what's required provides a breakdown of AUSTRAC's guidance.

In short, before 1 July 2026, AUSTRAC expects accountants providing designated services to:

- enrol as a reporting entity (the online enrolment system will be accessible from 31 March 2026)

- implement an AML/CTF program

- appoint an AML/CTF compliance officer

- train staff on their AML/CTF program and processes

- be ready to ask clients questions and report suspicious activity.

Tranche 2 entities should prepare for a significant review and update to their customer onboarding processes, risk management systems, and compliance procedures. In less than 12 months, these entities will need to:

- conduct know your client (KYC) checks

- monitor client transactions for suspicious activity

- conduct internal training on AML/CTF obligations

- monitor their compliance with their AML policies to report to AUSTRAC on a yearly basis.

AUSTRAC acknowledges the challenges newly regulated entities face in preparation for the reforms and has committed to facilitating the implementation of AML/CTF programs by providing ample guidance, education, and materials to such entities.

However, it is critical to note that non-compliance by newly regulated entities will be closely monitored by AUSTRAC from 1 July 2026 and will face intense scrutiny should ignorant or malicious non-compliance be encountered.

Concerns expressed by professional industry bodies

In response to AUSTRAC’s public consultation on the draft AML/CTF Rules, several professional industry bodies representing accountants have made submissions to AUSTRAC highlighting the concerns of their members regarding the new AML/CTF reforms.

Suspicious matter reports and personal safety

During the consultation process, concerns have been raised about the risks to the personal safety of practitioners when complying with AML/CTF obligations, particularly in the context of submitting a 'suspicious matter report' (SMR) in respect of a client/customer. From 1 July 2026, an accountant enrolled as a reporting entity will need to submit SMRs to AUSTRAC if they suspect, while providing designated services, a person or transaction is linked to criminal activity.

Concerns have been raised about the SMR obligation, as many accountants trade as small partnerships or sole practitioners which operate with fewer degrees of separation from their clients compared to, for example, larger financial institutions. This closer proximity often results in a deeper familiarity and understanding of the client’s personal and financial circumstances and increases the risk that a client may identify the accountant as responsible for lodging the report, raising legitimate fears around personal safety and retaliation.

Despite this, the AML/CTF Act, the draft Rules, and AUSTRAC guidance do not seem to include any relief or exemptions for accountants, where compliance with the Act or Rules may jeopardise their safety. CPA Australia suggested in their submissions that accountants should be exempt from submitting SMRs where ‘doing so would pose an unreasonable risk to your personal safety, or the safety of a member of your family or an at-risk staff member'[1]. These are the protections afforded to tax agents under different legislation.

References to Tax Practitioners Board (TPB) Codes

Submissions have also noted existing ethical and professional conduct codes imposing obligations upon accountants which overlap with obligations set out in the AML/CTF Act and Rules.

For example:

- The Rules require reporting entities to conduct due diligence on personnel engaged or hired as part of their business. However, accountants may already undertake similar checks under TPB(I) 41/2024 Code of Professional Conduct. CPA Australia has suggested that AUSTRAC should specifically reiterate in its guidance to accountants that there may be overlap between the AML/CTF obligations to conduct due diligence on personnel and similar obligations under existing codes applying to accountants.

- Similarly, when appointing an AML/CTF Compliance Officer, AUSTRAC applies a 'fit and proper person' test. CPA Australia has proposed that this test take into account existing requirements imposed on accountants by TPB(EP) 02/2010 Fit and proper person.

It remains to be seen whether AUSTRAC will respond to these industry-specific concerns raised in the consultation process. We note the final Rules are due to be released on 29 August 2025, and AUSTRAC will continue to release guidance on the Act and Rules on an ongoing basis.

Final comment

The AML/CTF regime in Australia remains a dynamic and evolving space, with the imminent reforms expected to have significant impacts on both existing regulated entities and Tranche 2 entities. If you’re unsure how these changes might affect you or your business, our AML/CTF experts are here to help. We would be happy to discuss your obligations and how to prepare.

[1] Section 15 of the Tax Agent Services (Code of Professional Conduct) Determination 2024.

Contact