Payroll tax risks for staffing businesses

Businesses that supply contractors to their clients, such as accountants, IT professionals, security personnel and medical staff, face significant payroll tax risks. These risks most commonly arise where the labour hire arrangement is classified as an employment agency relationship. In these circumstances, the worker is deemed to work for and within the client's business.

These provisions apply across a wide range of industry and business contexts, for both skilled or unskilled work, and for short or long-term engagements.

When does an employment agency relationship arise?

In broad terms, an employment agency relationship exists when a business procures workers for a client's business, and those workers perform their duties in and for the client’s business in much the same way as the client’s own employees. Typically, the workers will do so under the direction and control of the client.

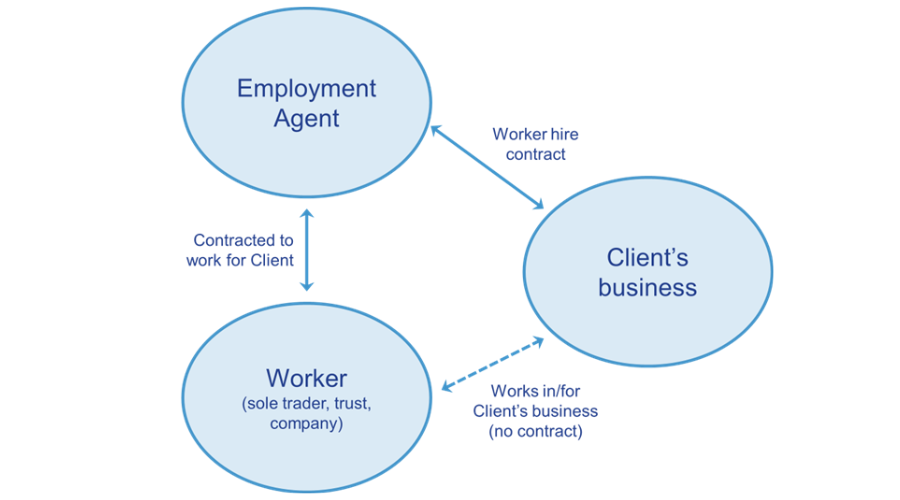

Under an employment agency, or labour hire arrangement, the labour hire business, as the service provider, contracts separately with the worker and with the client. There is no direct contract between the worker and the client.

In this scenario, the business supplying the worker is considered to be an employment agent and the worker’s employer for payroll tax purposes.

By contrast, if a separate contract is entered into between the client and the worker, as an employee or contractor of the client, then the employment agency rules do not apply. These types of arrangements are commonly referred to as placement arrangements and are typically entered into by recruitment agencies engaged to place workers with their clients.

Impact when an employment agency arrangement exists

Where an employment agency arrangement exists:

- the worker is deemed to be an employee of the employment agent regardless of the structure through which services are provided by the worker, for example via company, partnership or individual; and

- all payments made to, or on behalf of, the worker is deemed to be wages for payroll tax purposes.

The employment agency provisions apply in priority to the relevant contract provisions that exist in most states. As a result, exemptions often relied on in contracting scenarios – such as where the contractor provides their services to the public, or the engagement is for less than 90 days in a year – do not apply to exempt an employment agency arrangement from payroll tax.

The only (limited) exemptions that apply are where the wages deemed to be paid would be exempt from payroll tax had the client paid them directly to the worker as an employee. This may occur where the client is a not-for-profit body or a hospital, PBI, and the client has given the employment agent a declaration to that effect.

What businesses should do

Businesses that supply professional staff to clients should remain alert to the payroll tax risks associated with employment agency relationships. These risks can have significant financial implications, particularly if the arrangement is found to fall within the scope of the payroll tax employment agency rules.

State revenue authorities are devoting significant time and resources to identifying employment agency arrangements. To mitigate these risks, businesses should carefully review both new or existing staffing arrangements and seek professional advice to ensure compliance with payroll tax obligations. Taking these steps can help avoid unexpected liabilities and ensure that their operations remain compliant with relevant tax regulations.

Contact