Raising capital without a PDS: what listed funds need to know

ASX-listed registered schemes have several options for raising capital without issuing a product disclosure statement (PDS) (or prospectus, for funds that have a company within the stapled group) under the Corporations Act or obtaining securityholder approval under the ASX Listing Rules. These ‘low doc’ capital raisings can be commenced and completed relatively quickly when capital is required for acquisition or other purposes, and include:

- security purchase plans (SPPs);

- rights issues or entitlement offers; and

- institutional placements.

These can in each case be underwritten by one or more underwriters, and SPPs and rights issues are often undertaken immediately following an institutional placement.

Each raise structure has specific legal requirements that need to be complied with for issuers to have the benefit of disclosure document, securityholder approval, takeovers restriction exceptions and ASX listing rule timetables that need to be complied with.

A summary of the key regulatory exemptions and conditions for each raise structure is set out below.

| Disclosure and approval exemptions | Regulatory conditions |

|---|---|

Security purchase plans SPPs provide an option to raise capital from existing retail securityholders in a low-dilutive way. Each existing securityholder is offered securities up to a dollar value cap on a non-renounceable basis. | |

ASIC Corporations (Share and Interest Purchase Plans) Instrument 2019/547 provides relief from the requirement to issue a PDS. ASX Listing Rule 7.2 Exception 5 permits SPPs without securityholder approval as an exception to an entity’s placement capacity. However, the placement capacity exception does not apply to any underwrite of the SPP (which does not mean that they cannot be underwritten, but that placement capacity would be absorbed).

| Under the ASIC instrument, for disclosure relief to apply:

Under the Listing Rules, for securityholder approval and placement capacity relief to apply:

ASX also needs to be provided with, and approve, the SPP timetable for the raise. |

Rights / entitlement offer A rights issue or entitlement offer is an offer of securities made to existing securityholders to subscribe for new securities in the fund. The offer is made on apro-rata basis in proportion to the existing securityholdings and often allows securityholders to subscribe for any shortfall not otherwise taken up. Rights issues can be renounceable or non-renounceable and can adhere to the traditional timetable or be conducted on an accelerated basis. A renounceable rights issue involves the rights to subscribe for securities in the rights issue being quoted, such that existing securityholders can trade their rights if they do not take them up. A non-renounceable raise precludes trading in those rights. Under an accelerated rights issue, an institutional component of the offer is completed first, with the remainder of the offer period allowing for retail participation. A traditional or non-accelerated offer permits all securityholders to participate based on the same timetable. | |

Disclosure exemptions are available under sections 708AA (for shares) and 1012DAA (for units) of the Corporations Act, extended by ASIC Corporations (Non-Traditional Rights Issues) 2016/84. ASX Listing Rule 7.2 Exception 1 permits rights issues without securityholder approval as an exception to an entity’s placement capacity. Exception 2 permits an underwriter to take up the shortfall of a rights issue as an exception to placement capacity. Under section 611 (item 10) of the Corporations Act, the issue of securities to an existing shareholder or underwriter is an exception to the takeovers prohibition on acquiring interests above 20%. | Under the Corporations Act, for disclosure relief to apply, the rights issue must comply with the definition set out in section 9. This requires that:

The ASIC instrument also grants relief specific to ‘non-traditional’ rights issues (being accelerated rights issues, and the disposal of shortfall) etc. Under the Listing Rules, the key condition is that the offer is pro rata on the same terms for all securityholders. However, the Listing Rules expressly clarify that allowing participation in the shortfall (ie allowing securityholders to take up more than their pro rata allocation if available) and excluding participation outside of Australia and New Zealand will not disqualify the rights issue from meeting those requirements. |

Institutional placements Institutional placements offer a relatively flexible structure for raising within short timeframes from sophisticated investors and are often accompanied by a rights issue or SPP (to raise additional capital and provide existing securityholders with the opportunity to participate to reduce the dilutive impact). Institutional participants may be existing or new investors and may be selected for strategic purposes. | |

Disclosure exemptions are available under sections 708A (for shares) and 1012D (for units) of the Corporations Act. While there is no placement capacity exemption for institutional placements, securityholder approval for an additional 10% placement capacity (ie bringing the total to 25% of issued securities) can be obtained in advance, but only if the entity has amarket capitalisation of less than $300 million and is not included in the S&P/ASX 300 Index). | Under the Corporations Act:

Under the Listing Rule 7.1A, if approval is obtained from securityholders to rely on the additional 10% placement capacity (bringing it to 25%), securities must be issued at a price that is at least 75% of the VWAP for the 15 days trades were recorded prior to either the date on which the price is agreed with the institutional investor, or if that date is more than 10 trading days before the securities are issued, the date of issue. ASX approval will also be required if the fund needs to go into trading halt so that the bookbuild process can be undertaken by the lead managers. |

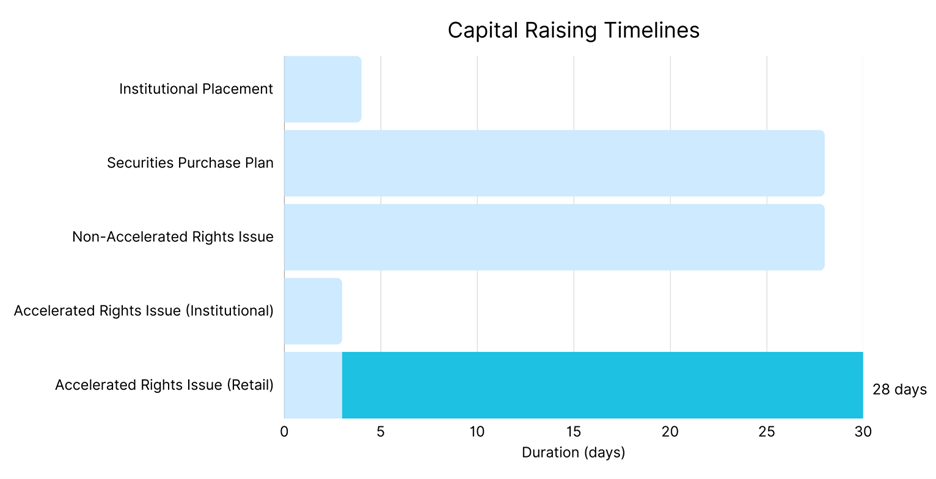

Timing

Timing is a key consideration for any listed capital raisings and another area that is regulated, particularly under the ASX Listing Rules. The following graph shows the estimated periods for completion of different capital raisings from the time of announcement:

Other considerations

In addition to the above conditions, issuers need to take into account:

- timing requirements (of both the managers/brokers and the regulators) and disclosure requirements when managing the capital raise process;

- compliance with unit pricing restrictions, which are addressed in more detail in our article Navigating unit pricing in listed fund capital raisings;

- third party financier approval requirements;

- related party transaction restrictions (under the Corporations Act and ASX Listing Rules); and

- in addition to any specific Chapter 6 exemptions, the guidance of the Takeovers Panel on the way capital raisings should be structured and conducted in light of control considerations.

For more information on listed capital raisings, please contact our team. If you would like more information about funds transactions – including capital raisings and mergers and acquisitions, please share your details if you would like to receive your copy of our Major funds transactions in Australia: a guide for fund managers which will be published soon.

Contact